You own a Chicago suburbs rental. The rent covers the mortgage, taxes, and insurance. But barely. Some months, you’re writing a check. You ask yourself: Should I hold, optimize, or sell? This guide walks you through the decision.

The Problem Everyone Avoids Talking About

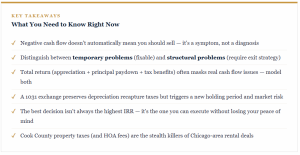

Negative cash flow is far more common than landlords admit in public. One bad refinance, a property tax reassessment, an unexpected HOA fee increase, or a rent-below-market tenant in year five — and suddenly your “investment” costs money every month.

The real challenge: negative cash flow is not the same as a bad investment. You might be building equity rapidly, capturing appreciation, receiving tax benefits, and generating a strong total return — all while writing a check every month. Conversely, a property with positive cash flow might be underleveraged, overtaxed, or sitting in a dead-market appreciation zone.

The question isn’t “Am I losing money?” It’s “Is this the best use of my capital and my peace of mind right now?”

Three Paths Forward — And Why Each Matters

Two Chicago Suburbs Scenarios Worth Thinking Through

Scenario A · Structural Problem

The Over-Leveraged Evanston Condo

Purchased in 2021 at near-peak prices with a 3.25% rate, then refinanced in 2023 to pull equity — now carrying a higher balance at 7.1%. HOA fees have increased. Taxes are $7,200/year. Rent is $1,950/month; PITI + HOA is $2,280/month. Negative $330/month.

The analysis: Appreciation has been flat in this specific building. HOA reserves are underfunded — a special assessment is possible. Refinancing won’t help at current rates. This is structural. A 1031 into a Midwest multifamily or a DuPage County single-family with better price-to-rent dynamics likely makes more sense than holding.

Scenario B · Fixable Problem

The Underrented Naperville Single-Family

Owned since 2017, low mortgage balance, 3.75% rate. Current tenant in year 6 at $1,800/month — never received a meaningful rent increase. Market comps show similar homes renting at $2,250–$2,400. Taxes are high but manageable. Monthly negative cash flow of $180/month.

The analysis: This property isn’t broken — it’s underoptimized. A professional market rent analysis, a tenant conversation at lease renewal, and modest cosmetic upgrades could swing this $400–$600/month positive. Selling or exchanging would mean giving up a well-positioned, low-leverage asset unnecessarily.

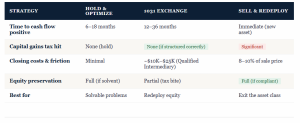

The Decision Framework: 5 Questions Before You Act

- Is the negative cash flow temporary or permanent? If it’s a one-time expense or a fixable management issue, hold and optimize. If it’s structural, you need an exit strategy.

- What is your total return, honestly? Factor in appreciation, principal paydown, and tax benefits. If total return is still positive even with negative cash flow, the math might support holding.

- What does the equity do for you elsewhere? If your $120,000 in trapped equity could generate meaningfully better returns in a different investment, that opportunity cost is real. Capital sitting in a flat-appreciation property is not free.

- What is your liquidity situation? Can you comfortably carry negative cash flow for 12–24 months if needed? An investor with strong reserves has options a leveraged investor does not.

- Is this affecting your quality of life? A property that costs you sleep, health, or relationship stability is worth more to sell than your spreadsheet might show. This is a legitimate factor.

“The best investment decision isn’t always the one with the highest IRR. It’s the one you can execute without losing your mind — or your peace of mind.”

A Note on Professional Guidance

This is not a decision to make alone or quickly. Before selling or initiating a 1031, you want three conversations: one with a CPA who specializes in real estate tax strategy, one with a financial advisor who can model the full portfolio impact, and one with a property management professional who can honestly assess what optimization is realistically possible for your specific property.

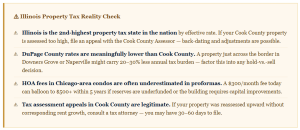

The Chicago suburbs market is nuanced. What’s true in a Cook County condo is different from a DuPage County single-family. Local expertise matters here in ways that generic national advice simply can’t account for.

This article is for informational purposes only and does not constitute financial, tax, or legal advice. All real estate investing involves risk, including potential loss of capital and property tax changes. Before making any investment decision — including a sale, 1031 exchange, or refinance — consult with a qualified CPA, financial advisor, and real estate attorney. Market data reflects conditions as of June 2026 and may have changed. Sources: Illinois Department of Revenue, IRS Publication 544, Cook County Assessor’s Office, Zillow Research, Federal Reserve Bank of Chicago, National Association of Realtors.